Deposit “Classic”

-

Intended Purpose: for resident and non-resident individuals.

AMD USD EUR RUB 100,000 - 100,000,000* 1000 - 300,000* 1000 - 300,000* 20,000 - 20,000,000* -

Interest payment procedure: monthly – to card/bank account days AMD USD EUR RUB 30 - 90 5.25% - - - 91 - 180 6% 0.25% - 0.5% 181 - 365 7.25% 2.5% - 0.5% 366 - 549 9.25% 3.55% 1.6% 3.5% 550 - 730 9.4% 4.0% 2.25% 4.5% Interest payment procedure: at the end of the term days AMD USD EUR RUB 30 - 90 5.5% - - - 91 - 180 6.5% 0.25% - 1.5% 181 - 365 7.5% 2.75% - 1.5% 366 - 549 9.5% 3.75% 2% 4% 550 - 730 9.7% 4.25% 2.5% 5% -

Interest payment procedure: monthly – to card/bank account

Interest payment procedure: at the end of the term -

Interest payment procedure: monthly – to card/bank account days AMD USD EUR RUB 30 - 90 5.38% - - - 91 - 180 6.17% 0.25% - 0.5% 181 - 365 7.5% 2.53% - 0.5% 366 - 549 9.65% 3.61% 1.61% 3.56% 550 - 730 9.82% 4.07% 2.27% 4.59% Interest payment procedure: at the end of the term days AMD USD EUR RUB 30 - 90 5.62% - 5.64% - - - 91 - 180 6.61% - 6.66% 0.25% - 1.51% 181 - 365 7.5% - 7.64% 2.75% - 2.77% - 1.50% - 1.51% 366 - 549 9.29% - 9.50% 3.72% - 3.75% 2% 3.96% - 4% 550 - 730 9.27% - 9.48% 4.16% - 4.21% 2.48% 4.88% - 4.94% -

* Interest rates for deposits exceeding the maximum amount are set on a contractual basis.

The deposit is a term deposit intended for resident and non-resident individuals.

Interest payments are made, at the depositor’s discretion, either at the end of the term or monthly, to the depositor’s bank or card account. Interest capitalization is not applied.

All depositors are provided with a UNIPAY unified utility payment system card as a gift.

For the Bank’s depositors and/or investors in the Bank’s bonds, the following payment cards are provided FREE OF CHARGE**, and no annual service fee is charged during the entire validity period of the card (3 years):

For amounts of AMD 1 million or equivalent foreign currency and more — VISA Classic, Mastercard Standard

For amounts of AMD 10 million or equivalent foreign currency and more — VISA Gold, Mastercard Gold

For amounts of AMD 20 million or equivalent foreign currency and more — VISA Signature, Mastercard World Travel

For amounts of AMD 50 million or equivalent foreign currency and more — VISA Infinite, Mastercard World Elite

**The rules for issuing and using payment cards are available on the official website of “UNIBANK” OJSC under Debit Cards — Unibank.

Tariffs and penalties

-

1. Term deposit accounts are serviced through bank accounts. If the client does not already have an account with “Unibank” OJSC, the Bank will open an AMD account for those making term deposits in AMD. For term deposits in foreign currency, the client can choose either a foreign currency account or an AMD account.

-

2. The annual maintenance fee for each account is 1,200 (one thousand two hundred) AMD for resident individual term depositors, 20,000 (twenty thousand) AMD for non-residents, and 500 (five hundred) AMD for resident individuals holding foreign currency accounts. Deposit account statements are provided free of charge once a month. A fee of 2,000 AMD is charged for duplicate statements for accounts less than 1-year-old, and 5,000 AMD for accounts over 1-year-old. The Bank reserves the right to close a customer's account unilaterally if the service fees specified in the Bank's tariffs are not paid, if the balance does not increase, or if no transactions have been made for over a year. For resident and non-resident individuals, the opening of each account in AMD, USD, EUR and RUB is FREE of charge. Deposit account statements are provided FREE of charge once a month.

-

3. In case of early termination of the deposit agreement at the request of the depositor:

a. the interest amounts already paid are deducted from the deposit principal,

b. interest is recalculated for the actual period the deposit was held in the Bank at the annual interest rate of a demand deposit set by the Bank, which amounts to 0.1% for AMD / USD / EUR / RUB currencies.

-

4. The term of the bank deposit agreement is extended as specified in the agreement. If the depositor does not re-quest payment of the deposit after the term expires, the agreement will either be extended under the terms outlined in the agreement, at the interest rate in effect at the time of extension, or the deposit amount will be transferred to the depositor's bank account, where the terms applicable to bank accounts will apply. The interest rate on the balances of bank accounts for resident and non-resident individuals, both in AMD and foreign currency, is 0% per annum for the actual period the deposit remains with the bank. The bank has the right to change the interest rate calculated on bank account balances in accordance with the rates and tariffs approved by the Executive Board of “Unibank” OJSC, unless otherwise provided for in the bank account servicing agreement.

-

5. Funds from third parties may also be deposited into the depositor's account in the depositor's name, with the nec-essary details about their deposit account provided.

-

6. The amount of interest on the Deposit specified in the Bank Deposit Agreement is not subject to unilateral reduction by the Bank during the term of the deposit.

-

7. Interest on funds in the deposit account is calculated based on the Nominal Interest Rate.

-

8. The annual percentage yield (APY) represents the interest a depositor would earn on a $1,000 deposit over a 365-day period, based on an annual simple interest rate with interest compounded and paid at regular intervals:

ATTENTION: INTEREST AMOUNTS ON THE FUNDS IN YOUR ACCOUNT ARE CALCULATED BASED ON THE NOMINAL INTEREST RATE. THE ANNUAL INTEREST YIELD SHOWS HOW MUCH INCOME YOU WILL RECEIVE AS A RESULT OF MAKING THE MANDATORY PAYMENTS RELATED TO THE DEPOSIT AND RECEIVING THE INTEREST AMOUNTS EARNED AT A DEFINED PERIOD. SEE BELOW FOR THE CALCULATION PROCEDURE FOR ANNUAL INTEREST YIELD

Information on interest rates

-

1. Annual simple interest rate - the annual interest rate set by the deposit agreement, based on which the bank calculates the interest payable to the depositor.

The formula for calculating interest paid under this type of deposit agreement:

DA * I/ 365 * Days – 10% (income tax), where

DA – Deposit Amount

I – Annual simple interest

Days –The number of days for the deposit is calculated based on Article 907, paragraph 1 of the Civil Code of the Republic of Armenia. According to this, interest on the deposit amount is calculated for the calendar days from the date the bank receives the deposit until the day before it is returned to the depositor or withdrawn for any other reason.

Example 1

Maturity period - 366 days

Deposit Amount - 1000 USD

Annual simple interest 4.25%

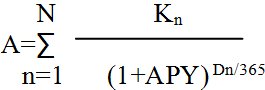

1000 * 4.25 /100 / 366 * 365 -10% = 38.25 USD2. Annual percentage yield (APY) - shows how much the annual interest rate on the deposit will be as a result of the customer making mandatory payments related to the deposit and adding the interest received to the principal amount (capitalization).

,where

,where

A - initial deposit amount,

n- serial number of cash flows on the deposit,

N- is the last number of cash flows for the deposit (including the cash flow at the time of deposit placement), after which the term of the deposit agreement is considered to have ended,

Kn - flows of the deposited amount and/or capitalized interest at the time of deposit placement and/or during the term of the deposit, as well as mandatory payment flows, if any,

Dn - is the number that shows how many days have passed from the date of deposit placement until the next (nth) cash flow made against the deposit, inclusive.In the case when the cash flow is at the time of deposit placement: D 1=0.

APY- is the annual percentage yield.

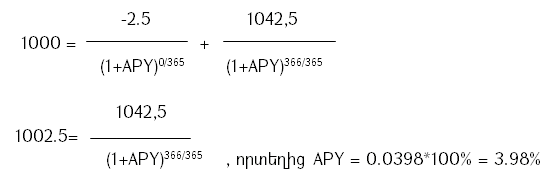

· Let's assume a deposit is offered with the following terms:

a. Deposit amount: 1000 USD

b. Maturity period: 366 days, 1 year

c. Annual simple interest: 4.25%

d. Interest payments at the end of the deposit term

e. Mandatory payments made by the depositor on the day of receiving the deposit:Mandatory deposit account maintenance fee: 1200 AMD /2.5 USD/ per year

The interest paid at the end of the term of the deposit agreement will be:

1000 * 0.042,5 = 4,25 USD

n = 1, n = 2

D1 = 0, D2 = 366

K1 = -2.5, K2 = 1042,5

3. Possible calculation of annual interest rate on deposits with regular interest payments:

APY = (1+r/n)n- 1, where

APY - Annual percentage yield

r - Nominal Interest Rate

n - the frequency of interest capitalization within a yearIf the frequency of interest payments at the end of the term is n =1, then

APY = (1+0.0425/1)1 -1,

APY = 0.0425*100 = 4.25%

Information on the protection of depositor rights

-

Disputes and disagreements arising from account servicing or the deposit agreement are resolved by mutual agreement. In case of failure to reach an agreement, the rights of the depositor are subject to protection in court, as well as through the financial system mediator. The depositor may protect their rights personally or through an authorized representative.

The bank does not have the right to condition the conclusion of a deposit agreement on the conclusion of an arbitration agreement.

Other information

-

1. The documents required to place a deposit are:

· a passport or another identification document;

· a Public Services Number (Social Security Card) or a certificate confirming refusal to obtain one;

· other additional documents as may be required by the Bank.

2. Interest is accrued on the amount of a term deposit from the date the deposit is received by the Bank until the day preceding the date of its return to the depositor or its withdrawal from the Depositor's deposit account on other grounds. Interest is accrued daily. If the deposit is invested in AMD, the interest payment is made exclusively in AMD, and if it is invested in a foreign currency, the interest payment is made at the choice of the Depositor, either in the currency of the invested Deposit, or in AMD, at the average exchange rate of the given day in the currency markets published by the Central Bank of the Republic of Armenia.

3. The interest accrued on the deposit is subject to income tax in accordance with the legislation of the Republic of Armenia, the rate of which is 10%. The depositor is paid the already taxed interest.

4. If the deposit repayment date coincides with a holiday and/or weekend, the deposit repayment date is considered the following business day.

5. If the Deposit is placed in the Bank in a foreign currency, then by signing the Agreement, the Depositor confirms that he/she is aware of the possible adverse consequences arising from changes in the foreign currency exchange rate and prefers to place the deposit in a foreign currency.

6. Deposits made in the Bank are guaranteed by the Deposit Guarantee Fund for Individuals in accordance with the legislation of the Republic of Armenia. The guaranteed deposit limits are as follows:

a) if the depositor has only a dram bank deposit in an insolvent bank, the amount of the guaranteed deposit is sixteen million Armenian drams;

b) if the depositor has only a foreign currency bank deposit in an insolvent bank, then the amount of the guaranteed deposit is seven million Armenian drams;

c) if the depositor has dram and foreign currency bank deposits in an insolvent bank, and the amount of the dram bank deposit exceeds seven million Armenian drams, then only the dram deposit is guaranteed, up to sixteen million Armenian drams,

d) if the depositor has dram and foreign currency bank deposits in an insolvent bank, and the amount of his dram bank deposit is less than seven million Armenian drams, then the dram bank deposit is guaranteed in full and the foreign currency bank deposit is guaranteed in the amount of the difference between seven million drams and the compensated dram bank deposit.

YOU HAVE THE RIGHT TO COMMUNICATE WITH THE BANK IN YOUR PREFERRED WAY: BY POSTAL OR ELECTRONIC. RECEIVING INFORMATION ELECTRONIC IS THE MOST CONVENIENT. IT IS AVAILABLE 24/7, FREE FROM THE RISK OF LOSS OF PAPER INFORMATION AND ENSURES CONFIDENTIALITY.

For the purpose of due diligence of the customer as defined by the RA Law "On Combating Money Laundering and Terrorism Financing", the Bank may request additional documents or other information from the consumer based on the "Know your customer" principle, as well as ask additional questions to the consumer during oral communication.

Contracts, agreements, partnerships or memberships concluded by the Bank may have a direct impact on depositors (for example, in accordance with the agreement concluded with the United States based on the Foreign Account Tax Compliance Act (FATCA), the Bank may collect additional information to determine your US taxpayer status).

Call Center: +37410 59 55 55 +37410 71 22 22

“Your Financial informant” - www.fininfo.am

ATTENTION: “YOUR FINANCIAL INFORMANT” IS AN ELECTRONIC SYSTEM WHICH MAKES IT EASY TO SEARCH, COMPARE, AND SELECT THE MOST EFFECTIVE OPTION FOR SERVICES OFFERED TO INDIVIDUALS.

Archive 07.07.2025

Archive 16.09.2024

Archive 01.12.2023

Archive 25.09.2023

Archive 05.04.2023

Archive 17.02.2023

Archive 21.11.2022

Archive 25.10.2022

Archive 15.09.2022

Archive 17.08.2022

Archive 28.06.2022

CALCULATOR

The calculations provided are approximate. Please, contact our specialists for more accurate information.

The calculations provided are approximate. Please, contact our specialists for more accurate information.

-

#CALCULATOR#

-

Information on interest rates

-

1. Annual simple interest rate - the annual interest rate set by the deposit agreement, based on which the bank calculates the interest payable to the depositor.

The formula for calculating interest paid under this type of deposit agreement:

DA * I/ 365 * Days – 10% (income tax), where

DA – Deposit Amount

I – Annual simple interest

Days –The number of days for the deposit is calculated based on Article 907, paragraph 1 of the Civil Code of the Republic of Armenia. According to this, interest on the deposit amount is calculated for the calendar days from the date the bank receives the deposit until the day before it is returned to the depositor or withdrawn for any other reason.

Example 1

Maturity period - 366 days

Deposit Amount - 1000 USD

Annual simple interest 4.25%

1000 * 4.25 /100 / 366 * 365 -10% = 38.25 USD2. Annual percentage yield (APY) - shows how much the annual interest rate on the deposit will be as a result of the customer making mandatory payments related to the deposit and adding the interest received to the principal amount (capitalization).

,where

A - initial deposit amount,

n- serial number of cash flows on the deposit,

N- is the last number of cash flows for the deposit (including the cash flow at the time of deposit placement), after which the term of the deposit agreement is considered to have ended,

Kn - flows of the deposited amount and/or capitalized interest at the time of deposit placement and/or during the term of the deposit, as well as mandatory payment flows, if any,

Dn - is the number that shows how many days have passed from the date of deposit placement until the next (nth) cash flow made against the deposit, inclusive.In the case when the cash flow is at the time of deposit placement: D 1=0.

APY- is the annual percentage yield.

· Let's assume a deposit is offered with the following terms:

a. Deposit amount: 1000 USD

b. Maturity period: 366 days, 1 year

c. Annual simple interest: 4.25%

d. Interest payments at the end of the deposit term

e. Mandatory payments made by the depositor on the day of receiving the deposit:Mandatory deposit account maintenance fee: 1200 AMD /2.5 USD/ per year

The interest paid at the end of the term of the deposit agreement will be:

1000 * 0.042,5 = 4,25 USD

n = 1, n = 2

D1 = 0, D2 = 366

K1 = -2.5, K2 = 1042,5

3. Possible calculation of annual interest rate on deposits with regular interest payments:

APY = (1+r/n)n- 1, where

APY - Annual percentage yield

r - Nominal Interest Rate

n - the frequency of interest capitalization within a yearIf the frequency of interest payments at the end of the term is n =1, then

APY = (1+0.0425/1)1 -1,

APY = 0.0425*100 = 4.25%

Information on the protection of depositor rights

-

Disputes and disagreements arising from account servicing or the deposit agreement are resolved by mutual agreement. In case of failure to reach an agreement, the rights of the depositor are subject to protection in court, as well as through the financial system mediator. The depositor may protect their rights personally or through an authorized representative.

The bank does not have the right to condition the conclusion of a deposit agreement on the conclusion of an arbitration agreement.

Other information

-

1. The documents required to place a deposit are:

· a passport or another identification document;

· a Public Services Number (Social Security Card) or a certificate confirming refusal to obtain one;

· other additional documents as may be required by the Bank.

2. Interest is accrued on the amount of a term deposit from the date the deposit is received by the Bank until the day preceding the date of its return to the depositor or its withdrawal from the Depositor's deposit account on other grounds. Interest is accrued daily. If the deposit is invested in AMD, the interest payment is made exclusively in AMD, and if it is invested in a foreign currency, the interest payment is made at the choice of the Depositor, either in the currency of the invested Deposit, or in AMD, at the average exchange rate of the given day in the currency markets published by the Central Bank of the Republic of Armenia.

3. The interest accrued on the deposit is subject to income tax in accordance with the legislation of the Republic of Armenia, the rate of which is 10%. The depositor is paid the already taxed interest.

4. If the deposit repayment date coincides with a holiday and/or weekend, the deposit repayment date is considered the following business day.

5. If the Deposit is placed in the Bank in a foreign currency, then by signing the Agreement, the Depositor confirms that he/she is aware of the possible adverse consequences arising from changes in the foreign currency exchange rate and prefers to place the deposit in a foreign currency.

6. Deposits made in the Bank are guaranteed by the Deposit Guarantee Fund for Individuals in accordance with the legislation of the Republic of Armenia. The guaranteed deposit limits are as follows:

a) if the depositor has only a dram bank deposit in an insolvent bank, the amount of the guaranteed deposit is sixteen million Armenian drams;

b) if the depositor has only a foreign currency bank deposit in an insolvent bank, then the amount of the guaranteed deposit is seven million Armenian drams;

c) if the depositor has dram and foreign currency bank deposits in an insolvent bank, and the amount of the dram bank deposit exceeds seven million Armenian drams, then only the dram deposit is guaranteed, up to sixteen million Armenian drams,

d) if the depositor has dram and foreign currency bank deposits in an insolvent bank, and the amount of his dram bank deposit is less than seven million Armenian drams, then the dram bank deposit is guaranteed in full and the foreign currency bank deposit is guaranteed in the amount of the difference between seven million drams and the compensated dram bank deposit.

YOU HAVE THE RIGHT TO COMMUNICATE WITH THE BANK IN YOUR PREFERRED WAY: BY POSTAL OR ELECTRONIC. RECEIVING INFORMATION ELECTRONIC IS THE MOST CONVENIENT. IT IS AVAILABLE 24/7, FREE FROM THE RISK OF LOSS OF PAPER INFORMATION AND ENSURES CONFIDENTIALITY.

For the purpose of due diligence of the customer as defined by the RA Law "On Combating Money Laundering and Terrorism Financing", the Bank may request additional documents or other information from the consumer based on the "Know your customer" principle, as well as ask additional questions to the consumer during oral communication.

Contracts, agreements, partnerships or memberships concluded by the Bank may have a direct impact on depositors (for example, in accordance with the agreement concluded with the United States based on the Foreign Account Tax Compliance Act (FATCA), the Bank may collect additional information to determine your US taxpayer status).

Call Center: +37410 59 55 55 +37410 71 22 22

“Your Financial informant” - www.fininfo.am

ATTENTION: “YOUR FINANCIAL INFORMANT” IS AN ELECTRONIC SYSTEM WHICH MAKES IT EASY TO SEARCH, COMPARE, AND SELECT THE MOST EFFECTIVE OPTION FOR SERVICES OFFERED TO INDIVIDUALS.

-